All About Cryptocurrencies - Part 1: Blockchain

Uncover the revolutionary power of blockchain in the world of cryptocurrencies. From its origin to its impact on finance, explore it all in our blog post.

Bitcoin is the buzzword of the decade. Even your grandma who knows nothing about investing has heard about it. But it can be very confusing and unintuitive to fully grasp it. Don’t worry, you are not alone. Around 80% of Malaysians are aware of cryptocurrencies, however, only 21% of them are actually familiar with it. Before you start investing in this unfamiliar territory - which is a classic recipe for a poor investment choice, you should: Invest in what you know. This article series is made to help you with that.

Tech is growing faster than ever and we need to keep up, and this article will equip you with crypto knowledge, regardless if you’re interested in investing or not (soon you will). It will help you save time and point you in the right direction of research. Where do we start?

The fundamental technology and platform of cryptocurrencies is the blockchain. Just as you can’t operate a car without its engine, cryptocurrencies wouldn’t exist or function without the underlying technology of blockchain. So, let’s dive into the technology first.

Origins: Where did it come from?

Blockchain can be dated back to the 1990s where Stuart Haber & W.Scott Stornetta, a group of research scientists, were finding a solution for time-stamping digital documents so they couldn’t be tempered or misdated with. No one furthered the progress of the blockchain into something revolutionary till…

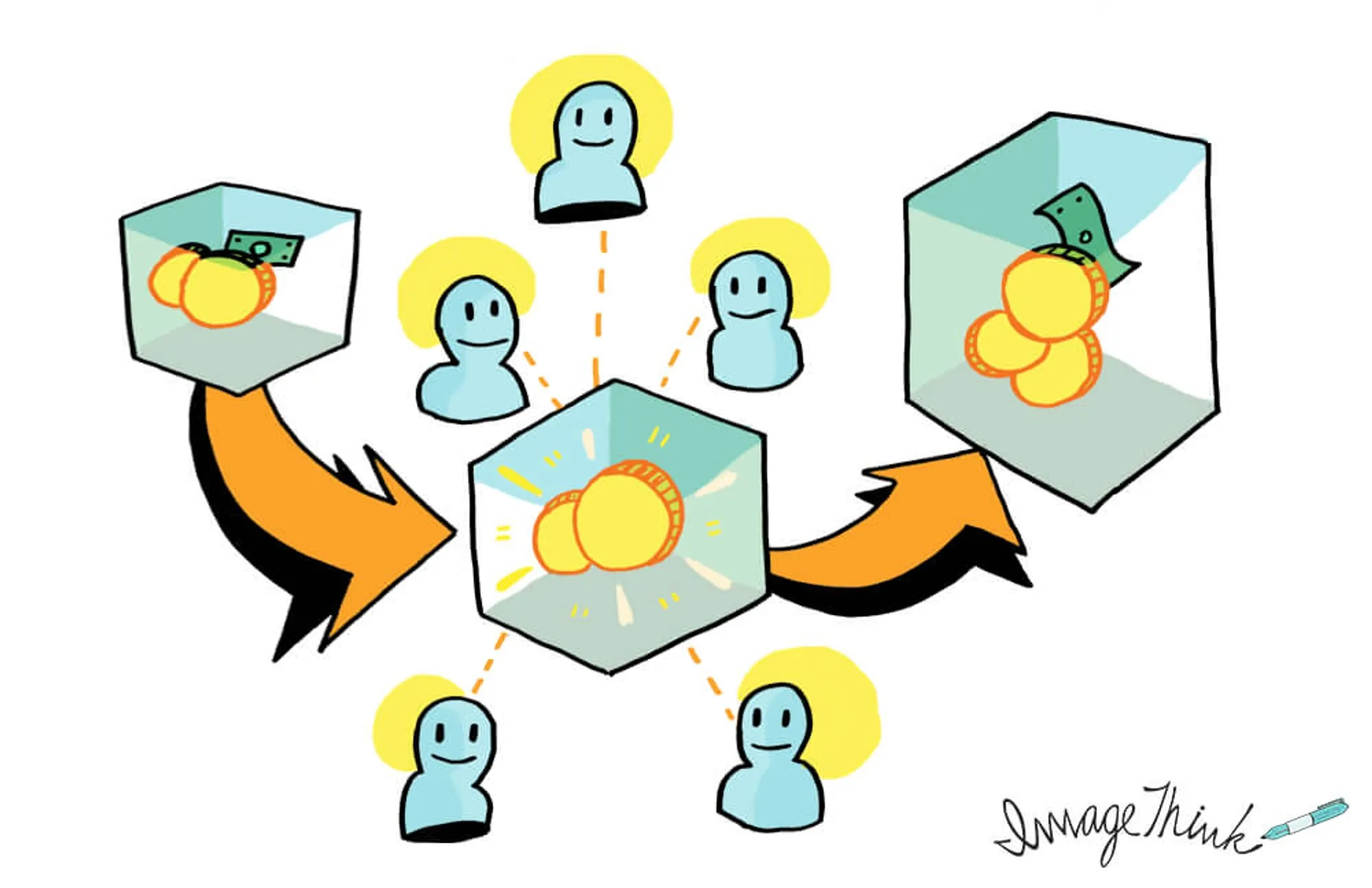

2008, where the concept of “Distributed Blockchain” was first introduced in the white paper “Bitcoin: A peer to peer electronic cash system” by Satoshi Nakamoto. The white paper described the vision and protocol of a decentralized financial system with no involvement of a financial intermediary. Basically, it’s a financial system where the middle man A.K.A the banks are removed and it’s purely a peer-to-peer transaction on a universal public ledger.

(A ledger is a collection of accounts where transactions are recorded. Every bank has its own record of ledger to keep track of the people’s money. Imagine, if there are around 44,000 banks with 44,000 ledgers of their own. Now, imagine, all those 44,000 ledgers are combined into one public-ledger where anyone can view.)

In 2009, Satoshi Nakamoto launched the first block of the Bitcoin blockchain: The Genesis Block.

And the rest is history.

What is a blockchain?

Essentially, blockchain is a decentralized database that stores a registry of assets and transactions across a peer-to-peer network. The transactions are secured through cryptography and over time, that transaction history gets locked in blocks of data that are cryptographically linked together and secure. This creates an immutable, unforgettable record of all of the transactions across this network (Bookmark this, we’ll explore it soon). This record is replicated on every computer that uses the network.

A great analogy given by Bettina Warbug, a blockchain researcher, to having a concept of Blockchain, is Wikipedia.

We can see everything on Wikipedia. Just as Wikipedia provides a dynamic and ever-evolving composite view of information, allowing users to track changes over time, blockchain serves as an open infrastructure for storing various types of assets. While Wikipedia stores words and images and their alterations over time, blockchain encompasses a broader spectrum, accommodating assets such as digital currencies like Bitcoin, intellectual property titles, certificates, contracts, physical assets, and even personal identifiable information, all while preserving their ownership, custodianship, and location history.

So why is it so important?

To illustrate the importance of blockchain, we must first understand the problem blockchain is solving.

The core problem blockchain aims to solve is: Trust. Trust in Institutions. But why?

Financial institutions act as intermediaries for our financial transactions, they are the heart of the economy, pumping and exchanging value. Just like an organism, it breathes the outflow and inflow of money and currency for society. We rely on institutions as a medium to manage our trade and reduce uncertainty. Especially with the rise of globalization, institutions are essential in facilitating human economic activity.

“Institutions are a tool to lower uncertainty so that we can connect and exchange all kinds of value in society”-Douglas North, Nobel Prize Winner in Economic Sciences.

Despite our trust upon institutions, there have been a record of 7 major financial crises over the last century. The most infamous incident of the 2008 financial crisis was the last straw that broke the camel’s back. Also known as the Global Financial crisis was the most severe economic crisis since the Great Depression 1929.

“The shock that hit the world economy in 2008 was on a par with that which launched the Depression.” - The Economist, University of Essex.

Blockchain as a confidence machine:

Blockchain is a confidence machine. Remember the bookmark from above? Immutable means it cannot be changed. All transactions in the blockchain cannot be erased and it is impossible for anyone to tamper with previous transactions.

These qualities are the basis of confidence in the blockchain. Confidence is returned back to society via the participation of the public network node to verify transactions by themselves and for themselves.

The blockchain’s decentralized and open-source approach to trust helps bridge the gap in information sharing among governments, businesses, and individuals. This model reduces information asymmetries and uncertainty in financial decisions.

Through the use of cryptography, blockchains establish a network of institutionalized trust, offering a viable alternative to the growing dependence on centralized entities which are controlling access to information.

Lastly

Companies from various industry sectors have been adopting this technology. Just to name a few: HSBC, Visa, Barclays, Ford, Pfizer, AIA and many more top leagues.

But they’re not using blockchain for cryptocurrency. That’s just the tip of the iceberg of the uses of block chain. Here is a list of other uses:

-

Providing an opportunity to developing nations to participate in banking (around 1.7 billion adults have no access to banking services)

-

Easing cross-border payments (average transaction fee for worldwide payments is 7%; yes, that’s a lot)

-

Increase in interoperability in the supply chain management

-

My favorite one: Managing and Protecting Patient data in Health care organizations. Imagine a decentralized log of patient data that is transparent and public for all hospitals to access. You don’t have to worry about switching hospitals or needing a specific doctor for record keeping. Your entire medical history can be accessed from anywhere, even globally.

There is much more to discover with this new technology. Do like the article if you want to know more about how blockchain can positively impact the World and also on the flip side, the negative implications of it (there is a shadow side for everything).

Subscribe to our financial newsletter for the latest news, insights, and advice on personal finance, investing, and more. With every email, you’ll gather the confidence and knowledge to make informed decisions to achieve your financial goals.