Everything You Need To Know About ASB Financing Loan

Here's everything you need to know about ASB Financing Loan and how it can benefit your ASB investment.

If you’ve heard of ASB, you’ve also probably heard of ASB Financing. But what’s the difference between these two and more importantly, which can make you more money?

What’s The Difference Between ASB and ASB Financing Loan?

ASB is a fixed-priced unit trust for Bumiputera Malaysians. In a way, you can consider it a “capital-guaranteed” and low-risk investment because its price is fixed at RM1/unit and only requires a minimum investment of RM10.

Historically since 19990 (inception), ASB average dividend returns are between 5%-14% p.a. which is pretty good, all things considered. Actually, if you’d like to know more about ASB and their other investment options (ASM & ASN) you can check out this article here.

In comparison, ASB Financing Loan is an alternative method to invest in ASB. This means, instead of cash investment (using your money to invest), you can borrow money from selected banks through a loan to finance your ASB investment.

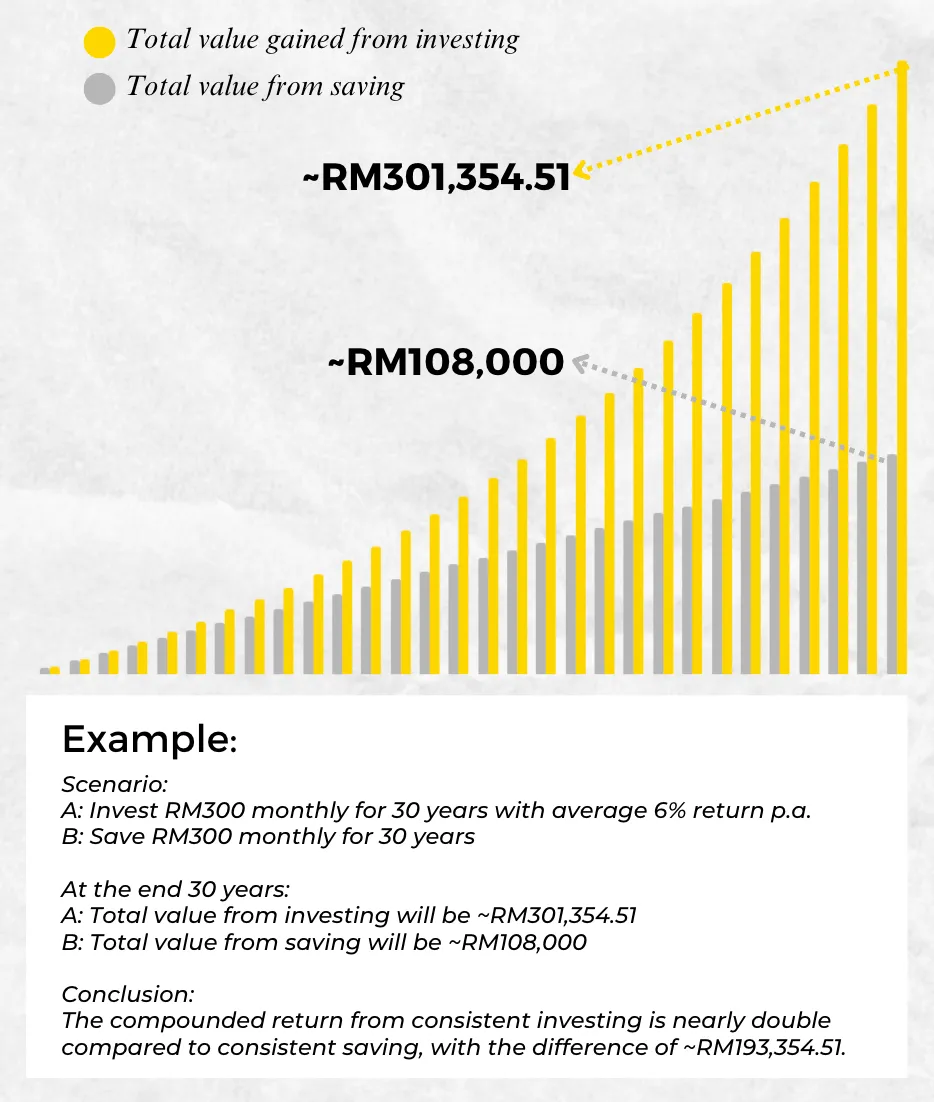

Harness The Power of Compounding With ASB Financing Loan

If you’ve been into investments long enough, you’ll eventually hear the phrase “the power of compounding” being thrown around a lot. Essentially what it means is to earn interest on both the initial amount of money invested and any interest already earned. Over time, this snowball effect can lead to an exponential growth of your money.

One of the ways to make full use of the compounding effect is to have a large initial investment capital; which is where ASB Financing Loan comes in handy if you don’t have that kind of capital on your own.

To better understand this, take a look at this example:

(BTW, this example was taken from our e-book, The 7 Steps Money-It-Right Framework.

If you want to get your hands on it, check out our website where you can sign up for our newsletter and you’ll get it for FREE!)

How Does ASB Financing Loan Work?

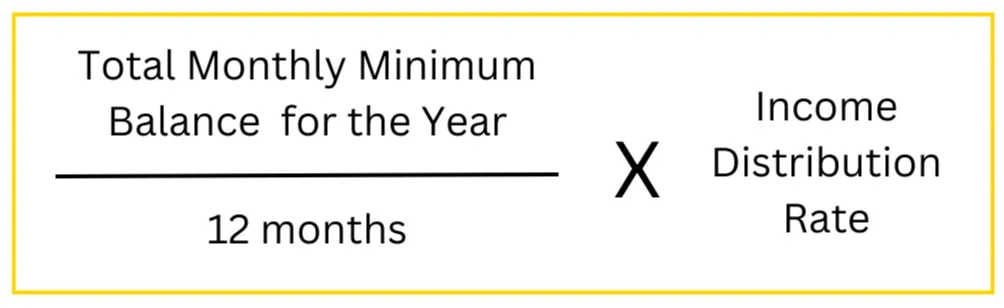

Firstly, you need to understand how ASB’s income distribution/dividend works. It’s based on this formula:

This means, if you have a larger average monthly minimum balance, you’ll be able to generate larger returns. And through ASB Financing Loan, it’s a sure-fire way of ensuring your average monthly minimum balance is a big amount.

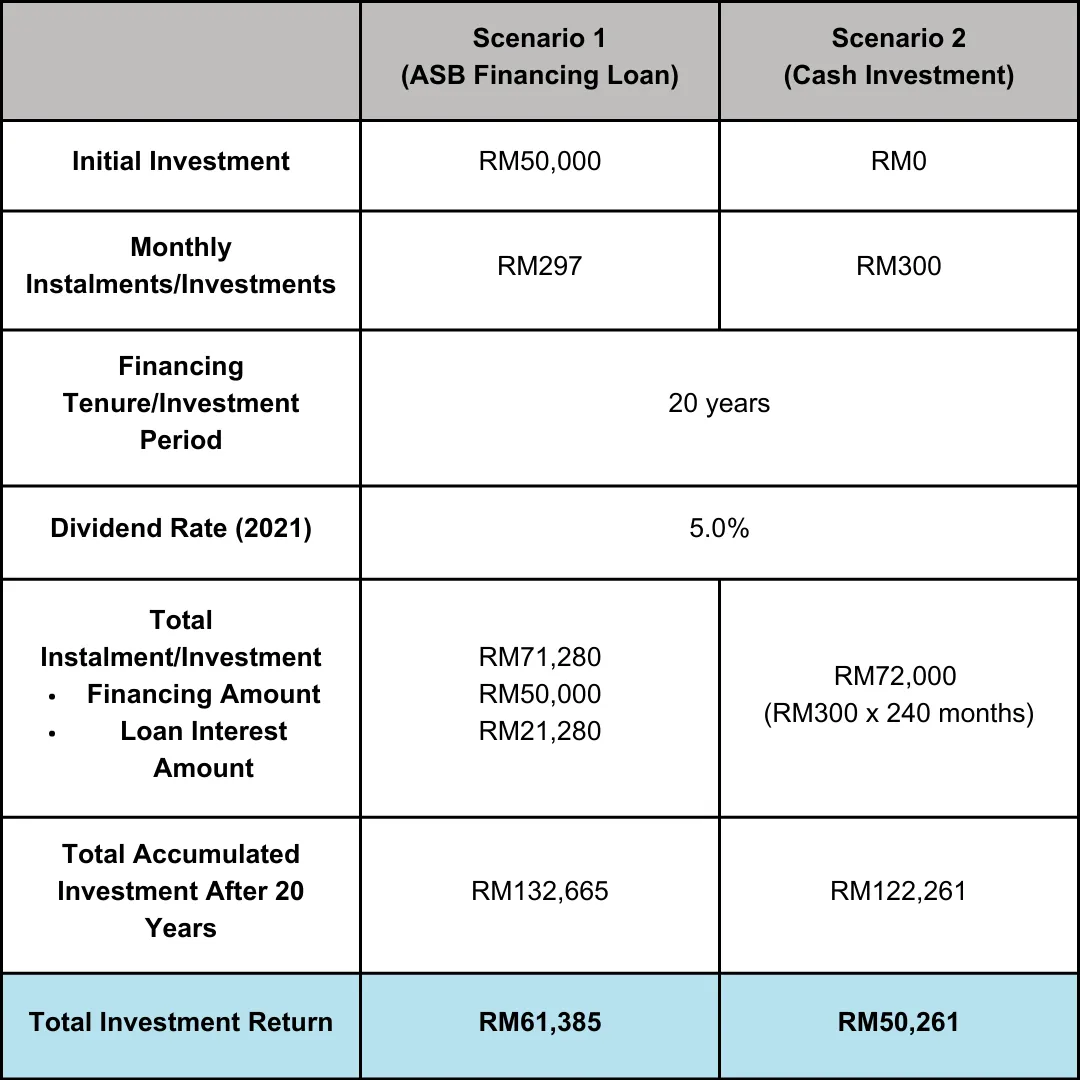

To have a clearer picture of this, let’s compare investing with ASB Financing Loan versus monthly cash investment:

Scenario 1:

You’re given RM50,000 in ASB Financing Loan with a financing rate of 3.5% for a tenure of 20 years.

Scenario 2:

You invest RM300 in cash investment every month for 20 years.

Therefore, with ASB Financing Loan, it gives you the ability to have a larger monthly minimum balance which will enable you to leverage on the power of compounding (and generate larger returns) without having to fork out a large capital investment on your own.

However, do note that since this facility functions like a regular loan, it’s not assured that you’ll even get the loan in the first place and if you do, you’ll have to repay the monthly instalments according to a financing rate (determined by the bank you’ve selected) for a fixed number of years which will affect your overall returns (offset your returns with the loan interest).

Tips And Tricks

-

Choose the bank that offers the lowest financing rate.

-

Retain the dividends to harness the power of compounding.

-

Subscribe to ASB Financing Loan takaful/insurance that protects your investment in the event of death or disability.

Pros and Cons of ASB Financing Loan

Pros

-

Allows you to have a large capital that will ensure a large average monthly minimum balance which can in turn, allow you to gain more in dividend returns.

-

Improve credit score if you’re disciplined with the monthly repayments.

-

Cultivates forced savings because you’re tied down to paying back the loan which is going into building your investment/savings.

Cons

-

ASB dividend rate is not fixed so there may be a chance that you’ll be servicing a higher financing rate for your loan (especially if there is a hike in OPR) in comparison to how much you’ll be earning through ASB’s dividends.

-

Can damage credit score if you fail to pay the monthly repayments.

-

Low liquidity because you can only withdraw ASB Financing Loan’s annual dividend in lump sum in comparison to conventional ASB cash investment where you can withdraw your money at any time.

How To Apply For ASB Financing Loan?

First, you’ll need to ensure that you’re eligible for it.

ASB Financing Loan Eligibility:

-

Malay or Bumiputera

-

Aged 18 years and above

-

Fixed income, minimum 3 months salary slip; if doing business, the company statement must be stated within 6 months

-

Not blacklisted by any bank including CTOS and CCRIS records

If you’re eligible for it, the next thing you’ll have to do is select a bank of your choice.

Here’s a list of banks you can apply to for ASB Financing Loan:

Once you’ve selected a bank, you’ll need to determine how big of a loan you’re allowed to borrow. This can be done by talking to the bank representative. Generally speaking, if your monthly salary is low, the financing loan offered will also likely be low. This is to ensure that you’re able to make the monthly repayments and not go into debt.

After that, you’ll need to prepare certain documents to proceed with the loan approval.

Required documents for ASB Financing Loan:

-

ASB Financing Loan application form

-

Photocopy of identity card (IC)

-

A copy of your bank statement or pay slip for the last three months

-

A copy of the front of the ASB account book

Our Verdict on ASB Financing Loan

Is ASB Financing Loan worth it? I would say it’s worth it but comes with some precautions.

This is mainly because of the fluctuating ASB dividend rate and loan financing rate. Currently, we find ourselves in an environment with rising interest rates. Naturally, this means the financing rate for the loan will increase as well. So now, we’re faced with a situation where we could be servicing more for the borrowed funds than we are earning from ASB.

However, based on past historical records, ASB has managed to ensure that their dividend is more than enough to cover the financing rate. For example, if we take a look at 1998, the average Malaysia OPR was 9.0% and yet, ASB was still able to provide dividend returns (including bonuses) of 10.50%. This goes to show that ASB is still relatively profitable and is able to give good returns to investors.

If you’re more of a watcher than a reader, we also made a video explaining ASB Financing Loan and it’s even in Bahasa Melayu! You can watch it here.